Lalit Shastri

How Indian law decisively separates capital investment from share ownership

Introduction: When Popular Definitions Enter Legal Territory

Ask Google the difference between an investor and a shareholder, and the answer sounds simple and intuitive: an investor is anyone who puts money into an asset for returns, and a shareholder is a specific type of investor who buys shares in a company. This explanation is widely circulated, commercially convenient, and perfectly acceptable in everyday financial discussions.

The confusion begins when this popular, market-oriented definition is applied to legal disputes. Indian courts have consistently held that while a shareholder may be described as an investor in common financial parlance, company law applies a far more precise and consequence-driven test. The distinction is not semantic. It directly affects how courts decide issues relating to taxation, insolvency, regulatory compliance, capital formation, and allegations of funding or control.

This article explains why courts do not rely on popular definitions, how securities premium is treated in law, and why a shareholder—despite paying a premium or buying shares from the open market—may still not qualify as an investor in the company.

Courts do not ask whether money was paid. They ask where the money went.

The Popular Definition—and Why Law Treats It with Caution

In finance and accounting literature, an investor is broadly understood as any person who deploys capital with the expectation of returns. Under this understanding, a shareholder is naturally described as an investor who has chosen equity as the investment vehicle. This usage is neither inaccurate nor misleading within its intended context. It works well for portfolio management, stock-market education, accounting classifications, and valuation exercises commonly undertaken by professional accountants.

However, courts are not concerned with descriptive convenience. They are concerned with legal consequences. When disputes arise, judges do not ask how a term is commonly used in the market. They ask whether a transaction resulted in legally recognisable effects under company law. This is where popular definitions stop being helpful and, if uncritically adopted, become misleading.

The Legal Test Courts Consistently Apply

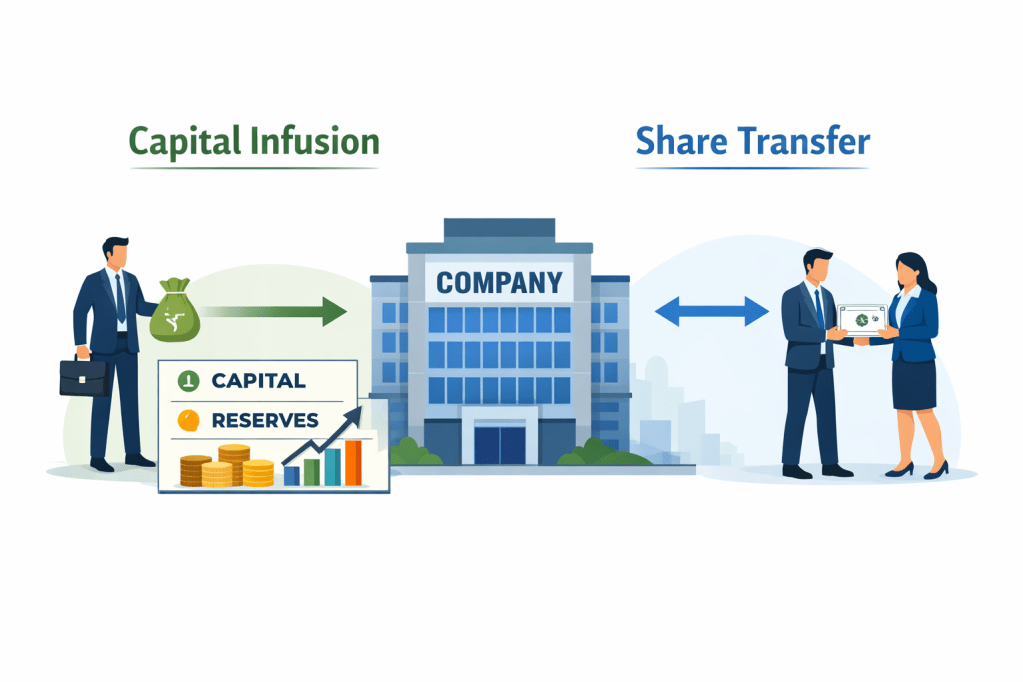

Across Supreme Court and High Court judgments, one test appears with striking consistency. Courts examine whether a transaction resulted in funds being infused into the company itself. If money flowed into the company and augmented its capital or reserves, the person providing that money may be treated as an investor in the company. If the money merely changed hands between private parties, the transaction is treated as a transfer of ownership, not an investment in the company.

This capital-centric test is the cornerstone of Indian company law jurisprudence. It is absent from popular definitions, but it is decisive in courtrooms.

In law, investor status follows capital infusion, not ownership change.

Securities Premium: What the Law Actually Says

A recurring misconception is that securities premium somehow remains “linked” to the shares for which it was originally paid, and that when those shares are transferred, the premium notionally travels with them. Indian courts have rejected this idea repeatedly and unequivocally.

The Supreme Court, in Bacha F. Guzdar v. Commissioner of Income Tax (1955), held that a shareholder has no ownership interest in the assets or reserves of the company. The company is a separate legal entity, and its capital and reserves belong exclusively to it. This principle applies with full force to securities premium.

The position was further clarified in CIT v. Standard Vacuum Oil Co. Ltd. (1966), where the Supreme Court held that share premium, once received by the company, becomes part of its capital structure and does not create any enforceable right in favour of shareholders. In legal terms, securities premium is a company-level statutory reserve. It is not share-specific, it is not shareholder-specific, and it does not migrate when shares are transferred.

A change in the register of members records a change in ownership of shares. It does not reallocate or reattribute capital reserves.

Securities premium belongs to the company—not to the shareholder, past or present.

Issue of Shares and Transfer of Shares: A Fundamental Legal Divide

Indian jurisprudence draws a sharp and consistent distinction between the issue of shares and the transfer of shares. When a company issues shares, consideration flows into the company, capital and premium are created, and the company’s financial resources are strengthened. This is capital formation.

When shares are transferred, the company receives nothing. The transaction occurs entirely between private parties, and the company’s capital structure remains unchanged. This distinction was authoritatively articulated by the Supreme Court in Sri Gopal Jalan & Co. v. Calcutta Stock Exchange Association Ltd. (1964), where the Court held that a company receives consideration only at the time of issue of shares, and that subsequent transfers are matters between shareholders with which the company has no concern.

The same principle was reaffirmed in Vodafone International Holdings BV v. Union of India (2012), where the Supreme Court observed that transfer of shares results in a change in ownership of the company, not a transfer of the company’s assets or reserves.

Are Open-Market Buyers Investors in the Company?

From a market perspective, open-market purchasers are often described as investors, including in reports and analyses prepared by professional accountants. From a legal perspective, courts have consistently taken a narrower view.

The Delhi High Court, in Trishul Investments Ltd. v. Commissioner of Income Tax (2008), held that purchase of shares from existing shareholders does not result in any funds being available to the company and therefore cannot be regarded as capital contribution. The buyer may have invested money, but that investment was in a security, not in the company’s capital.

This reasoning has also been echoed in insolvency jurisprudence. The NCLAT, in Union of India v. Infrastructure Leasing & Financial Services Ltd. (2019), observed that investor status flows from funding the entity, not merely from holding its securities.

Thus, an open-market purchaser may be an investor in securities or financial instruments, but not an investor in the company itself.

Buying shares may change ownership. It does not change the company’s finances.

The A–B Illustration That Clarifies the Law

Consider a common factual situation. A person subscribes to shares issued by a company at face value plus premium, and the premium is credited to the securities premium account. Some time later, that person sells the same shares to another buyer at the same price. The buyer pays exactly what the first holder paid, but the entire amount goes to the seller. The company receives nothing.

In law, the first holder is both a shareholder and an investor, because his transaction resulted in capital and premium flowing into the company. The second holder is undoubtedly a shareholder, because his name is entered in the register of members. However, he is not an investor in the company, because his payment did not result in any capital infusion. The historical fact that the company once received premium does not convert the later transfer into an investment.

The destination of funds, not their quantum, determines investor status.

Register of Members: What It Proves—and What It Does Not

The register of members is conclusive evidence of shareholding. It determines voting rights, dividend entitlement, and legal ownership of shares. It does not allocate reserves, attribute securities premium, or transform transferees into capital contributors.

This limitation was recognised by the Supreme Court in Howrah Trading Co. Ltd. v. Commissioner of Income Tax (1959), where the Court clarified that shareholding reflects legal title to shares, not ownership of company funds or reserves.

Reconciling Google, Professional Accountants, and the Courts

There is no need to declare popular definitions or professional accounting usage as “wrong”. Each serves a different purpose. Google’s definition reflects how markets and individuals commonly speak. Professional accountants often adopt commercially convenient terminology for reporting and analysis. Courts, however, apply legally binding tests rooted in statutory consequences.

When legal rights, liabilities, or allegations are in issue, judicial doctrine prevails over popular or professional usage.

Market language explains behaviour. Law determines consequences.

Why the Debate Ends Here

Indian courts have spoken with clarity and consistency. Securities premium is a company-level reserve and does not follow shares. Capital formation occurs only at the time of issue, not on transfer. Share transfers—even at a premium—do not amount to investment in the company. Open-market purchasers are shareholders, but not investors in the company.

Popular definitions may simplify understanding for the public. Courts, however, decide cases on where capital flows—not on what we casually call it.

That distinction is now well settled.