Lalit Shastri

The arrest of a Joint Director and senior Technical Assistant, both posted in the office of DG (Corporate Affairs), Ministry of Corporate Affairs(MOCA), and another Joint Director of MOCA posted as Official Liquidator, Corporate Bhawan, Chennai and an associate of a Mumbai based private company in a bribery case by the CBI in July 2023, had amply exposed the working of the Union Ministry of Corporate Affairs and the way many senior officers in the Ministry of Corporate Affairs, especially in the Office of Director General Corporate Affairs, were indulging in corruption while enforcing the provisions of the Companies Act, 2013.

The CBI had seized large amounts of cash and incriminating documents from the premises of the arrested officers is ample proof that they were indulging in corruption on a continuous basis, and the case in question was not a one-time exception.

Former director general of corporate affairs B K Bansal, who was facing a Central Bureau of Investigation (CBI) probe in a corruption case, had committed suicide along with his son, at their residence in East Delhi in September 2016.

B.K. Bansal, along with another person, was arrested for allegedly receiving Rs.9 lakh as bribe. The money changed hands outside a Delhi hotel.

In July 2016, the wife and daughter of B.K. Bansal were found hanging in their New Delhi flat.

These grim episodes gave me reason to go on a fact-finding mission vis-à-vis the enforcement of the Companies Act, 2013, by the Ministry of Corporate Affairs officials.

Section 447 of the Companies Act, 2013 is a penal provision. It was introduced for the first time in the Companies Act of 2013. It had no corresponding provision in the earlier Companies Act 1956. When it first became operative on 12th September 2013, Section 447 was not cognizable. It was explicitly made cognizable only by the amendment to Section 212 (6) by the Companies (Amendment) Act 2015 with effect from 25th May 2015.

The Finance Act of 2018 was later brought in to amend the Companies Act, 2013. With the Amendment of Section 212 (6), fraud under Section 447 of CA, 2013 attracting punishment as per Section 488, was made a cognizable offence on 25 May, 2015.

Following amendments in the Prevention of Money-laundering Act, 2002 (PMLA) through Finance Act, 2018, Corporate frauds also have been included as Scheduled offence – with the result, violation of provisions under Section 447 of the Companies Act, 2013 is a scheduled offence under PMLA so that the Registrar of Companies in suitable cases is able to report such cases for action by Enforcement Directorate under the PMLA provisions.

The officers of the Ministry of Corporate Affairs, who enforce the Companies Act, 2013, are supposed to keep in focus both the letter and spirit of the law governing companies. A comprehensive and detailed study of the Chapters and Sections dealing with Inquiry, Inspection, and investigation into complaints of fraud and misappropriation of funds by companies shows in no uncertain terms that the law-makers have paid full attention towards ensuring extraneous reasons and vested interests do not play any role and there is zero interference with the autonomous working of the enforcement authorities at different levels. To meet this end, their roles and powers have been well-defined for impartial and objective responses to complaints against companies.

Considering the havoc that can be caused to unsuspecting and law abiding enterprises and companies by interfering, vitiating and subverting the process under the Companies Act,2013, especially the process of Inspection under Sections 206, 207 and 208, enforcement of these provisions must be steel jacketed to ensure no one is in a position to manipulate the system through the submission of illegal Supplementary Reports.

When the Companies Act, 2013 provides for Inquiry, Inspection, and Investigation, why manipulate the process through Supplementary Inspection Reports is the big question?

Suppose the Ministry of Corporate Affairs is not satisfied with any Inspection Report, which is submitted under Section 208 and marks the culmination of the entire process of Inspection under Section 206 of the Companies Act, 2013. In that case, the Ministry still has the option to order an Investigation under Section 210 of the Act. Under this Section, The Central Government can appoint inspectors to investigate the company’s affairs and report on their findings. The Central Government can also assign an investigation to the Serious Fraud Investigation Office (SFIO). Mark it, the Companies Act, 2013 does not provide even an iota of ground to the Ministry to dictate or instruct the RD & IO what to write in the Inspection Report or the final Report submitted after the Investigation.

The sections devoted to the two reports (Section 208 and Section 223 of the Companies Act, 2013) – one after Inspection and the other during and after Investigation are crystal clear and these should be read together to understand the letter and spirit of the Act. The irony is that the clear difference between the two Sections is being fudged by Supplementary Inspection Reports by senior Ministry officers who think they can never be held accountable.

Section 208: Section 208 of the Companies Act, 2013 requires the Registrar or inspector to submit a written report to the Central Government after inspecting a company’s books and papers. The report may include: Documents, Recommendations for further investigation, and Reasons for the recommendations.

Section 223(1): An inspector appointed under this Chapter may, and if so directed by the Central Government shall, submit interim reports to that Government, and on the conclusion of the investigation, shall submit a final report to the Central Government.

There is no provision for a Supplementary Report under Section 208 the Companies Act, 2013.

Section 208 of the Companies Act, 2013, leaves no room for ambiguity. Section 208 “requires the Registrar or inspector to submit a report” (which means just one report). Whereas under Section 223, Inspectors appointed under the Act, if so directed by the Central Government shall, submit interim reports to the Government and on the conclusion of the investigation, shall submit a final report.

Section 447 on Punishment for Fraud.— Without prejudice to any liability including repayment of any debt under this Act or any other law for the time being in force, any person who is found to be guilty of fraud, shall be punishable with imprisonment for a term which shall not be less than six months but which may extend to ten years and shall also be liable to fine which shall not be less than the amount involved in the fraud, but which may extend to three times the amount involved in the fraud: Provided that where the fraud in question involves public interest, the term of imprisonment shall not be less than three years. Explanation.—For the purposes of this section— (i) ―fraud in relation to affairs of a company or anybody corporate, includes any act, omission, concealment of any fact or abuse of position committed by any person or any other person with the connivance in any manner, with intent to deceive, to gain undue advantage from, or to injure the interests of, the company or its shareholders or its creditors or any other person, whether or not there is any wrongful gain or wrongful loss; (ii) ―wrongful gain‖ means the gain by unlawful means of property to which the person gaining is not legally entitled; (iii) ―wrongful loss‖ means the loss by unlawful means of property to which the person losing is legally entitled.

Section 206 of the Companies Act deals with Power to call for information, inspect books and conduct inquiries.— (1) Where on scrutiny of any document filed by a company or on any information received by him, the Registrar is of the opinion that any further information or explanation or any further documents relating to the company is necessary, he may by a written notice require the company— (a) to furnish in writing such information or explanation; or (b) to produce such documents, within such reasonable time, as may be specified in the notice.

Under Section 206(4) of the Companies Act, 2013, the Central Government may, if it is satisfied that the circumstances so warrant, direct the Registrar or an inspector appointed by it to carry out an Inquiry.

Under Section 206(5) of the Companies Act, 2013, the Central Government may, if it is satisfied that the circumstances so warrant, direct inspection of books and papers of a company by an inspector appointed by it for the purpose.

Section 207 of the Companies Act, 2013 relates to the Conduct of inspection and inquiry.— (1) Where a Registrar or inspector calls for the books of account and other books and papers under section 206, it shall be the duty of every director, officer or other employee of the company to produce all such documents to the Registrar or inspector and furnish him with such statements, information or explanations in such form as the Registrar or inspector may require and shall render all assistance to the Registrar or inspector in connection with such inspection. (2) The Registrar or inspector, making an inspection or inquiry under section 206 may, during the course of such inspection or inquiry, as the case may be,— (a) make or cause to be made copies of books of account and other books and papers; or (b) place or cause to be placed any marks of identification in such books in token of the inspection having been made. (3) Notwithstanding anything contained in any other law for the time being in force or in any contract to the contrary, the Registrar or inspector making an inspection or inquiry shall have all the powers as are vested in a civil court under the Code of Civil Procedure, 1908 (5 of 1908), while trying a suit in respect of the following matters, namely:— (a) the discovery and production of books of account and other documents, at such place and time as may be specified by such Registrar or inspector making the inspection or inquiry; (b) summoning and enforcing the attendance of persons and examining them on oath; and (c) inspection of any books, registers and other documents of the company at any place.

After Section 447 of the Companies Act, 2013 became a penal provision when it was introduced for the first time in the Companies Act of 2013 and was made a cognizable offence on 25 May, 2015, and amendments were made in the Prevention of Money-laundering Act, 2002 (PMLA) through Finance Act, 2018 to include Corporate frauds as a Scheduled offense, it has been noticed that the letter and spirit of the Companies Act, 2013 has been blown to the winds by the enforcement authorities, from top to the Regional Director and RoC levels.

The purpose of Section 207 is to ensure impartiality in Inspection and that is why the law-makers have given the Inspecting officer the powers of a civil court under Section 207(3), which makes the IO a quasi-judicial authority. Hence the process of Inspection which begins with the Ministry ordering Inspection under Section 206(5) of the Companies Act, 2013 culminates with the submission of the Inspection Report under Section 208 of the Companies Act of 2013.

Section 208, which deals with Report on Inspection made, is categorical in underscoring that “The Registrar or inspector shall, after the inspection of the books of the account or an inquiry under section 206 and other books and papers of the company under section 207, submit a report in writing to the Central Government along with such documents, if any, and such report may, if necessary, include a recommendation that further investigation into the affairs of the company is necessary giving his reasons in support.”

It is evident from Section 208 of the Companies Act, 2013 that there is no provision for any supplementary inspection report. It only speaks about submitting a report in writing to the Central Government along with such documents, if any, and such a report may include a recommendation that further investigation into the affairs of the company is necessary giving his reasons in support.

Independent and exclusive inquiry has revealed that Supplementary Reports are being submitted by RD & IO to the Ministry on instructions of senior officers that too after the submission of the Inspection Report by the RD & IO under Section 208 of the Companies Act, 2013. The RD & IOs are also being instructed what to write in these reports. This amounts to total subversion of the entire process under the Companies Act, 2013 by the officials of the Ministry of Corporate Affairs. Submission of Supplementary Reports after Inspection is beyond the scope as mandated by Section 208 of the Companies Act, 2013 and issuing instructions and directing the RD & IO what to write in these reports amounts to compromising the objectivity and fair outcome of Inspections as the RD & IO, who is a quasi-Judicial authority during the course of Inspection cannot be told what to write in the Inspection Report.

RTI application by this author addressed to the Ministry of Corporate Affairs has opened up the Pandora box. The Ministry had forwarded my RTI application to all RDs and ROCs across India.

In response to the information sought under RTI for the following:

1. Please provide a certified copy of the particular Section under the Companies Act, 2013 that gives the power to the Registrar of Companies (ROC) or a Regional Director to submit a Supplementary Inspection report after the Inspection Report is submitted to the Central Government under Section 208 of the Companies Act, 2013.

2. Provide certified copies of all Supplementary Inspection reports submitted to the Central Government by the Registrar of companies (ROC) or a Regional Director between 1st January 2000 and 30th September 2024

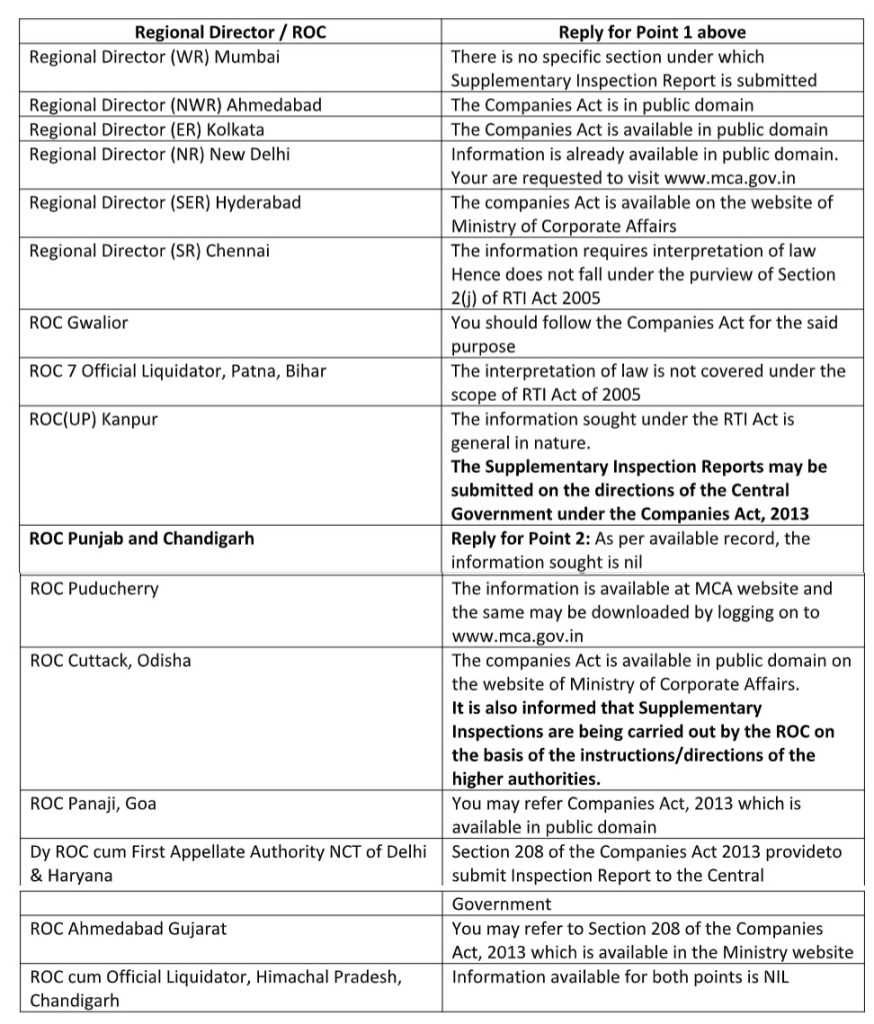

The replies from RD (NWR), Ahmedabad, and RD WR, Mumbai, other RDs and ROCs are as follows:

Reply from RD(NWR):

1. Reply for point no.1 – The Companies Act is in public domain at-

https://www.mca.gov.in/content/mca/global/en/acts-rules/ebooks.html. Which can be viewed by anyone.

2. Reply for point no. 2 – The Information as sought for is exempted under Section 8(1)(h) of the RTI Act 2005. Hence, the information cannot be provided.

While responding to the RTI application, RD(NWR), Ahmedabad, has failed to provide the Section of the Companies Act, 2013 under which the Supplementary report can be submitted after Inspection of books of Accounts, other books, and papers.

Many other ROCs and RDs have stated for Point 2 of my RTI application that under Section 8(1)(h) of RTI Act, the said information (copies of Supplementary reports) are exempted from disclosure. Some have even stated that sharing this information will adversely affect prosecution.

While others have stated that information for point 1 is available on Ministry website and the document ( The Companies Act, 2013) can be downloaded. What’s most baffling is that one has been advised by several authorities of the Ministry of Corporate Affairs to download the Act from the Ministry website, whereas it has no provision for a Supplementary Inspection Report. It has also been stated in a reply that Point 1 relates to interpretation of law (question arises, whether the enforcement authorities are supposed to enforce the law or interpret the law).

The Registrar of companies Kanpur has even gone to the extent of stating that Supplementary Inspection Reports may be submitted on the directions of the Central Government under the Companies Act (without mentioning in specific terms under which Section of the Companies Act, 2013 the Supplementary Inspection Report can be submitted after the submission of a Report on the conclusion of Inspection)

These replies notwithstanding, the reply of RD (WR), Mumbai, leaves no room for interpretation or speculation:

RD(WR), Mumbai, has stated in his reply for Point 1: “There is no specific Section under which a Supplementary Inspection Report is submitted.“

Reply from RD WR,Mumbai

On the RTI application seeking the following:

- a certified copy of the particular Section under the Companies Act, 2013 that gives the power to the Registrar of Companies (ROC) or a Regional Director to submit a Supplementary Inspection report after the Inspection Report is submitted to the Central Government under Section

208 of the Companies Act, 2013, and - Certified copies of all Supplementary Inspection reports submitted to the Central Government by the Registrar of companies (ROC) or a Regional Director between 1st January 2000 and 30th September 2024

Replies that have come from the Regional Directors, and RoCs are given in table below:

It is important to note that while on the one hand, the RD, Mumbai says, There is no specific Section under which Supplementary Inspection Report is submitted, the ROC, Ahmedabad refers to Section 208 of the Companies Act, 2013 and RD, Ahmedabad vaguely points to the Companies Act, 2013.

What stares us in the face is that Supplementary Inspection Reports are being submitted by the ROC on the basis of instructions/directions of higher authorities. Obviously therefore, this should be treated as a subversion of the entire process under the Companies Act, 2013 and a high-level probe should be ordered by the Central Government into this matter. Even the higher judiciary should take suo moto cognizance and initiate action against this.